January 17, 2024

Durable CDR Market Outlook: 2024 and Beyond

Preface

CDR.fyi’s mission is to accelerate durable carbon dioxide removal (CDR) worldwide. We launched the 2024+ Market Outlook Survey to provide an understanding of where the industry is in the short (2024), medium (2030), and long (2050) term.

We are confident the findings presented in this Summary Report will help add to the knowledge and insight in the industry and contribute to accelerating durable carbon removal worldwide.

If you have any questions or want to be included in future surveys, email us at team@cdr.fyi or connect with us on LinkedIn.

Happy reading!

Highlights

- Today's buyers are motivated to help accelerate the industry. Early development of the nascent carbon removal sector was the dominant motivation for buying, mentioned by 83% of purchasers.

- Purchasers are willing to pay. In 2024, 80% of purchasers are budgeting over $100 per tonne for durable CDR, a price 67% still expect to pay by 2050.

- Suppliers see costs coming down. 65% of suppliers think their production costs will be lower than $100 per tonne in 2050, up from 30% today.

- Suppliers are scaling to meet anticipated demand. By 2030, 93% expect to exceed 10,000 tonnes, with a third projecting 1M or more tonnes sold. By 2050, 70% project to sell more than 1M tonnes annually.

- And purchasers plan to buy more CDR. In 2024, 76% of purchasers will purchase under 10,000 tonnes. By 2050, over 55% of purchasers project to purchase over 25,000 tonnes and 17% over 1M tonnes.

- Clearer standards and lower prices are key for growth. 58% of purchasers chose declining prices, along with the establishment of clear standards, as the major contributors to buying more in the future.

- Access to financing and policy are the biggest risk factors. Suppliers mention access to financing (68% of respondents) and policy/regulatory challenges (60%) as the top risk factors that may endanger their growth.

- Buyers and suppliers want to transact directly: 60% of buyers want to purchase directly from suppliers, and over 80% of suppliers say their main sales channel is direct. Marketplaces are the secondary channel most expected to increase in importance.

Purchaser Insights

The primary purpose of the Purchaser Survey was to gain perspective on current and future demand, pricing, and requirements. With these insights, suppliers can better plan their capacity, create their business projections, and secure financing to establish and scale their facilities.

As a foundational starting point, it is apparent there is an escalating commitment to durable CDR among the respondents, rising from an already high ~50% of buyers reporting 75-100% allocation in 2024 to 75% by 2050.

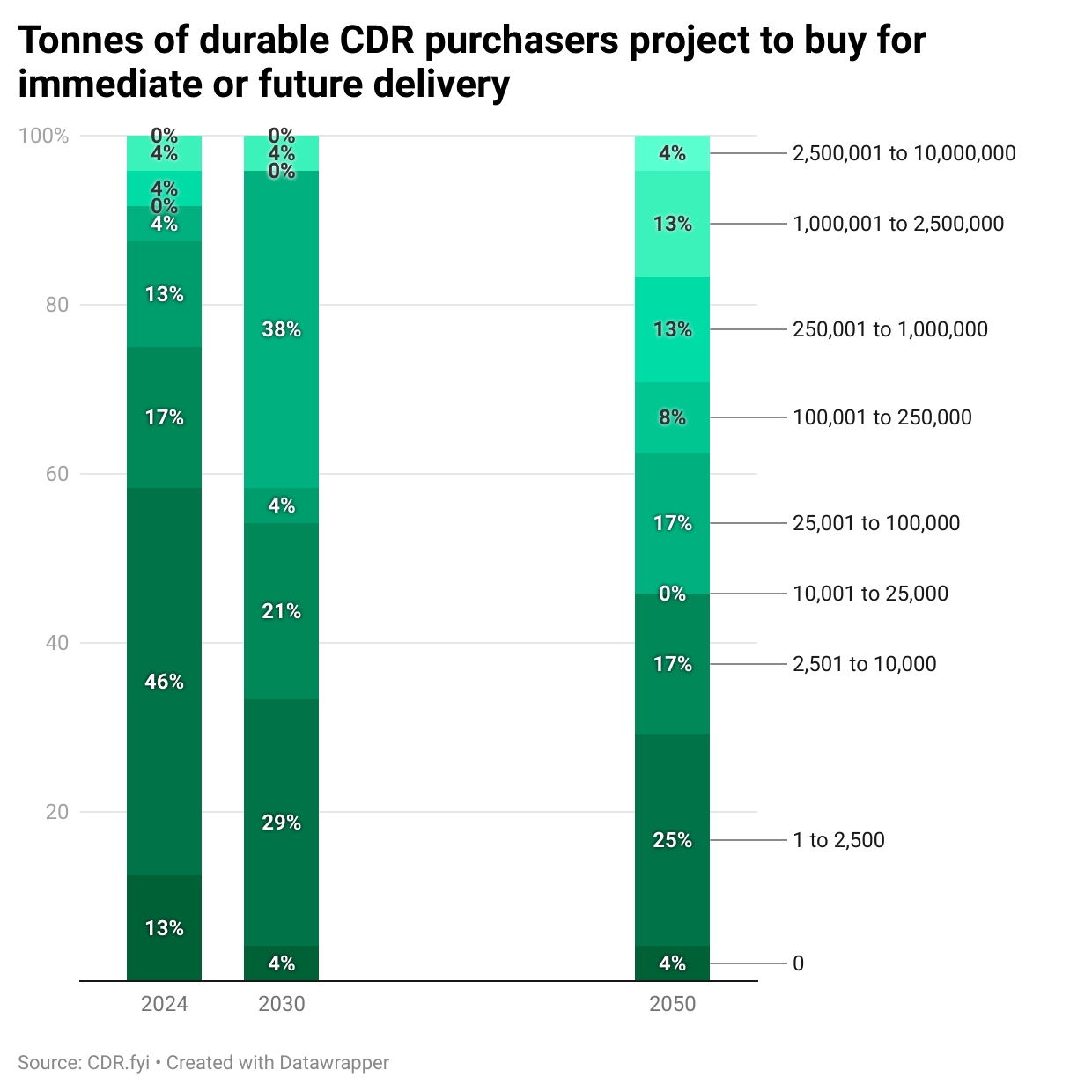

A key question we posed was to ask purchasers to provide ranges of their projected procurement volumes in 2024, 2030, and 2050. In the figure below, the 2024 bar reflects the nascent market, with 76% of purchasers stating that they had purchased 10,000 tonnes or less and 46% only 1 to 2,500 tonnes. By 2030, the bulk of responses shift to the 25,001 to 100,000 tonne range, and by 2050, over 55% of purchasers project to be purchasing over 25,000 tonnes, and 17% over 1M tonnes.

Price expectations

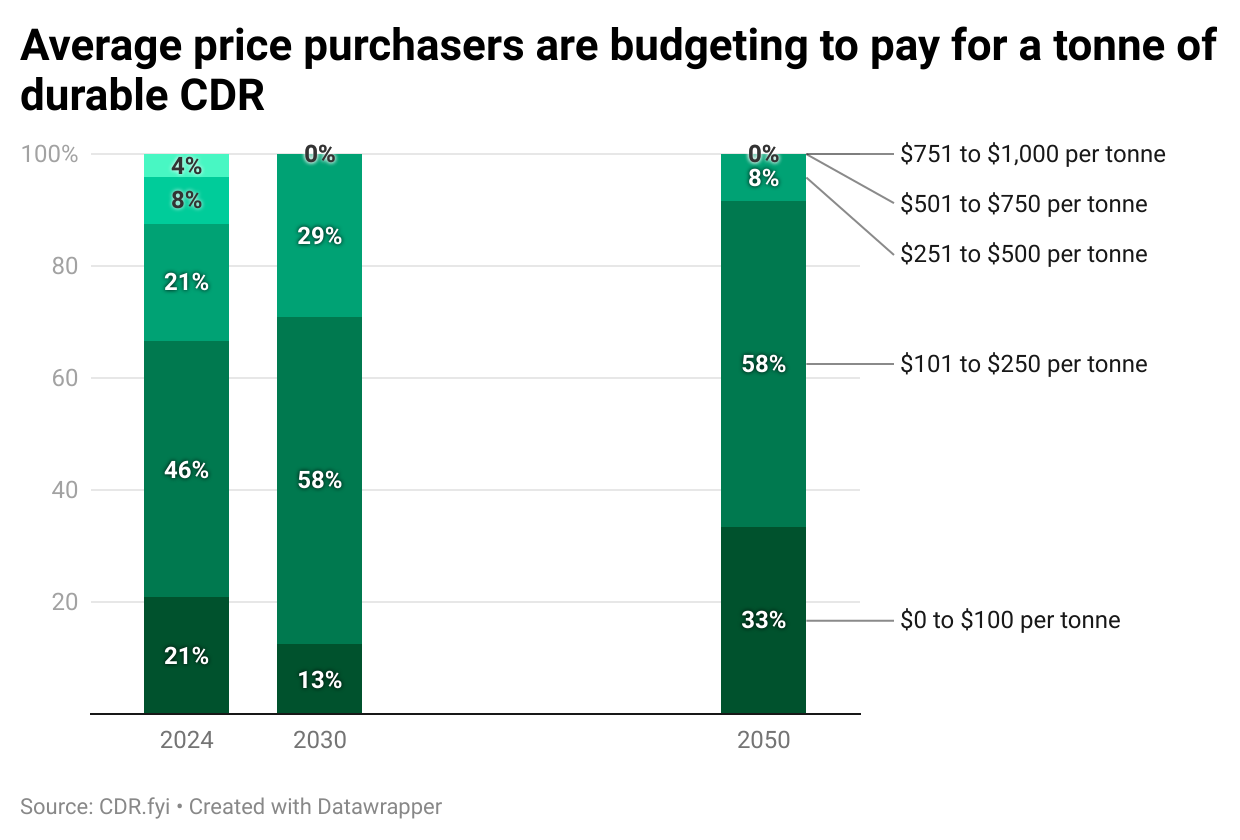

The other key element of transactions we covered was pricing. There is a strong willingness to pay for durable CDR: in 2024, 79% of purchasers budgeted over $100 per tonne for durable CDR. Although purchasers expect prices to decline as efficiency, productivity, and volumes increase, 67% still expect to pay $101 to $500 per tonne in 2050.

The current and future price expectations contrast markedly with the $5 - $10 range in the voluntary carbon markets for less durable carbon credits, indicating that purchasers are willing to pay more for higher durability. As methods and supplier capacity scale, we expect to see the prices of credits from durable CDR decline but maintain a premium based on perceived quality rather than experience race-to-the-bottom commodity dynamics.

Requirements

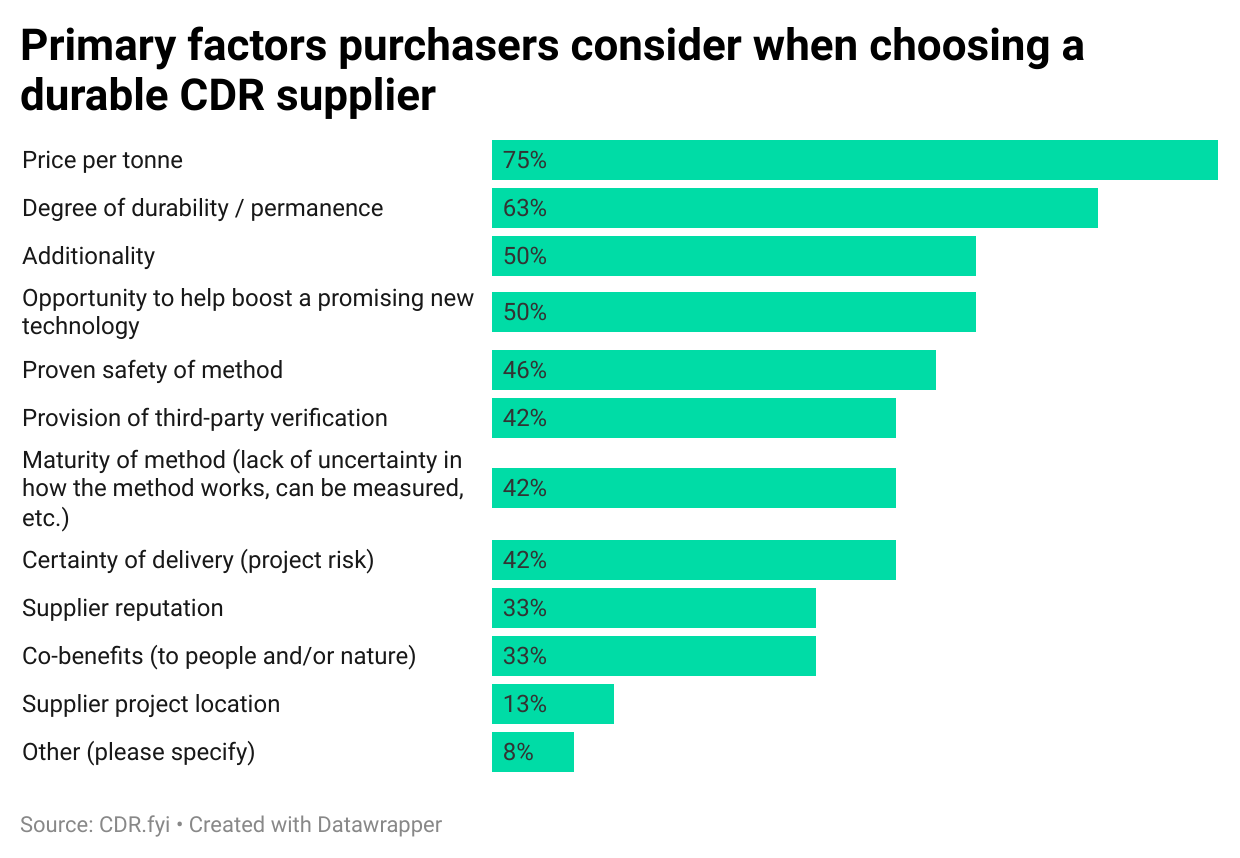

Price is the main factor that purchasers consider, but not the only one. When asked what they value in choosing suppliers, 75% of respondents selected price per tonne as a primary factor. The other major factors can be separated into three major groups: quality, reliability, and market seeding.

The importance of quality as a primary factor for consideration is demonstrated by over 60% of respondents selecting the degree of permanence and 50% selecting additionality. The supplier's reliability comes into focus as seen by the selections of the proven safety of the method, third-party verification, maturity of the method, and certainty of delivery, with all four of those factors being selected by between 40% and 50% of respondents. Finally, market seeding comes in high, with the opportunity to help boost a promising new technology tied for the third highest factor selected at almost 50%.

Net, price, quality, and reliability are at the top, but the prominence of market seeding demonstrates the responsibility that early purchasers are taking on to aid in progressing the category.

Motivations

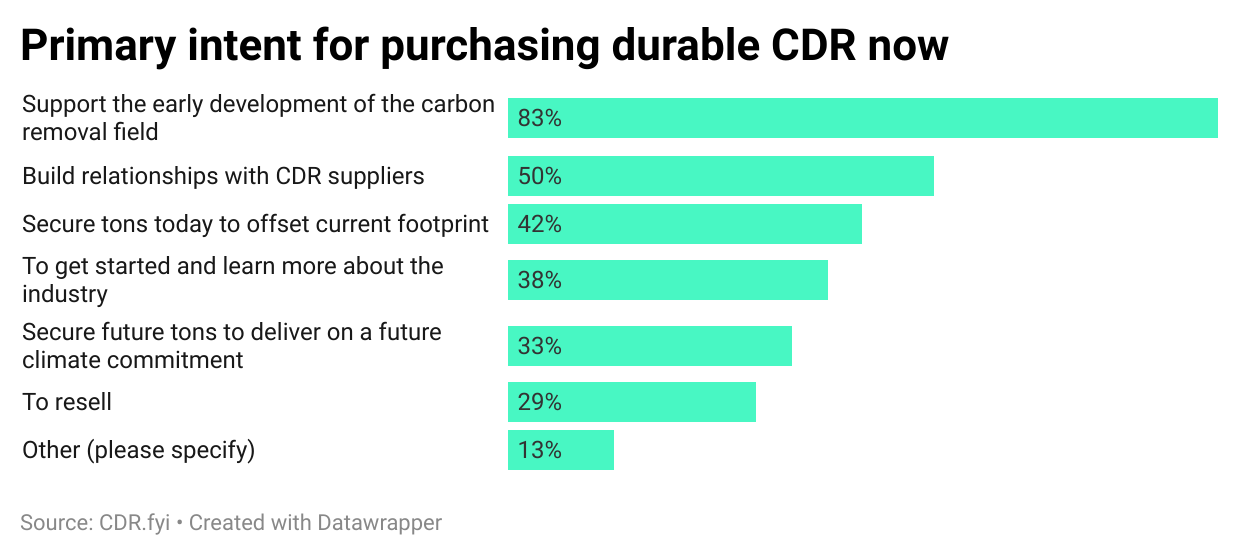

Why are companies purchasing durable CDR? Related to our last point about progressing the category, the dominant motivation mentioned by 83% of respondents is supporting the early development of the nascent carbon removal sector. Most early participants see climate impact through sector development as the primary driver rather than solely offsetting their value chain footprints. It also confirms durable removal's standing as an emerging opportunity for first movers to shape.

Another notable indication of investment in the future of the sector, and in particular the company’s access to future durable CDR, can be seen by their prioritizing building relationships with suppliers (50%), and getting started to learn more about the industry (38%). Purchasers show moderate intent on securing durable CDR tonnes today to offset the current carbon footprint, with that motivation being mentioned by 42% of respondents.

One of the “Other” respondents demonstrated a particularly proactive approach to future guidance, stating their intention to “anticipate SBTi allowances in net zero targets.”

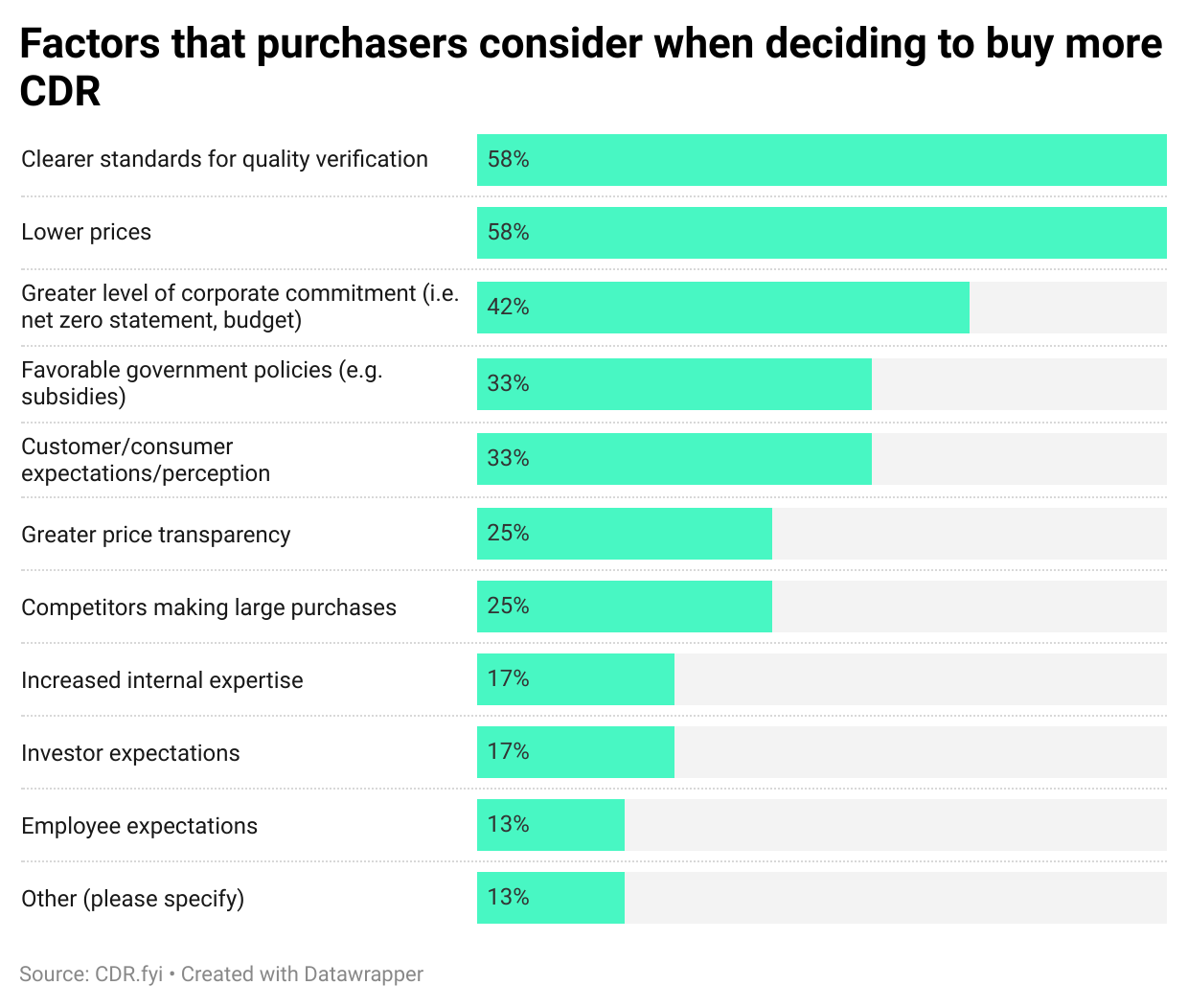

What would increase purchasers’ motivations to buy more durable CDR? Lower prices and clearer verification standards (58% of respondents for each) come in at the top, indicating that reducing costs and boosting confidence are keys to catalyzing scale-up. Increased corporate commitment, supportive government policies, and positive public perceptions are secondary drivers, selected by 42% (for the first) and 33% (for the latter two) of respondents. “Clarity around carbon accounting principles” was called out by one of the “Other” respondents.

Channels

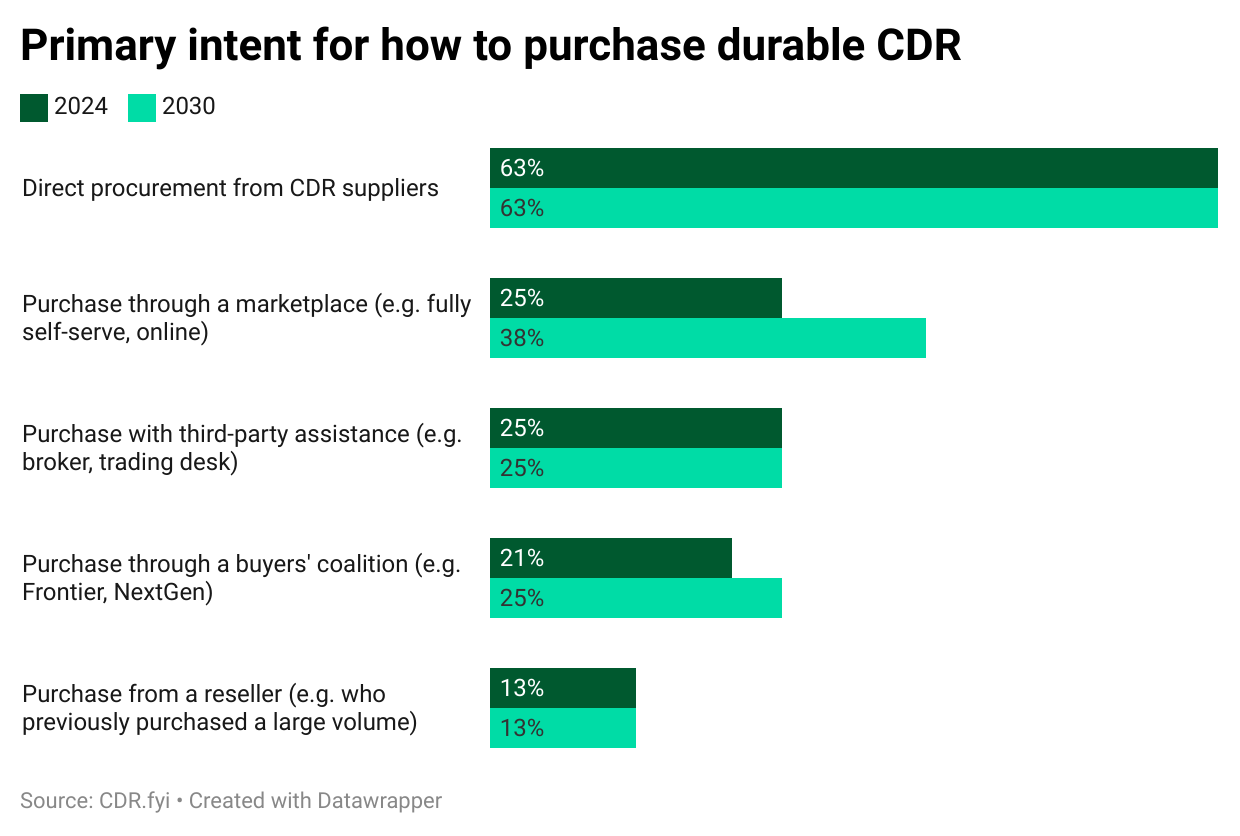

What channels are purchasers using to purchase their durable CDR? The most common approach, both for 2024 and expected for 2030, is direct procurement from suppliers, mentioned by 63% of respondents. Marketplaces were the second-most selected option at 25% in 2024, trending upward to 38% by 2030. A challenge for marketplaces today is that the vast majority of purchases are for future delivery, which complicates the business models of intermediaries. The fact that all options displayed will be stable to increasing from 2024 to 2030 reflects the increased volume of purchasers making their way through the various channels.

Durable CDR Methods

Asking what purchasers plan to buy yields a diverse result. The most popular category is biochar (67% of respondents), followed by enhanced weathering (58%), direct air capture (54%), and biomass carbon removal and storage (42%). By 2030, most categories show moderate changes, indicating a diversified but relatively stable preference set based on currently available information.

Supplier Insights

Sales - Historical and Projected

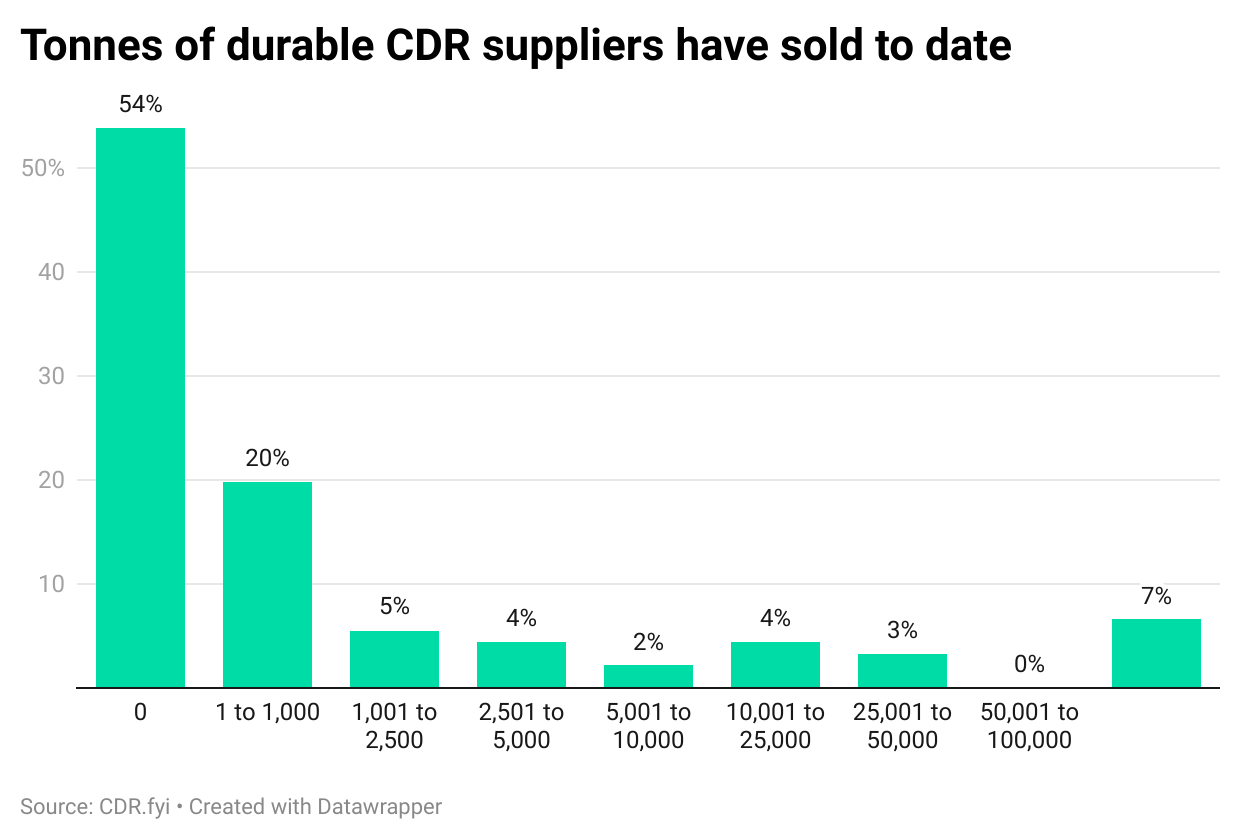

Given the early-stage profile of the companies, it is unsurprising that over half of them (54%) reported no sales to date, with 74% reporting volumes under 1,000 tonnes sold.

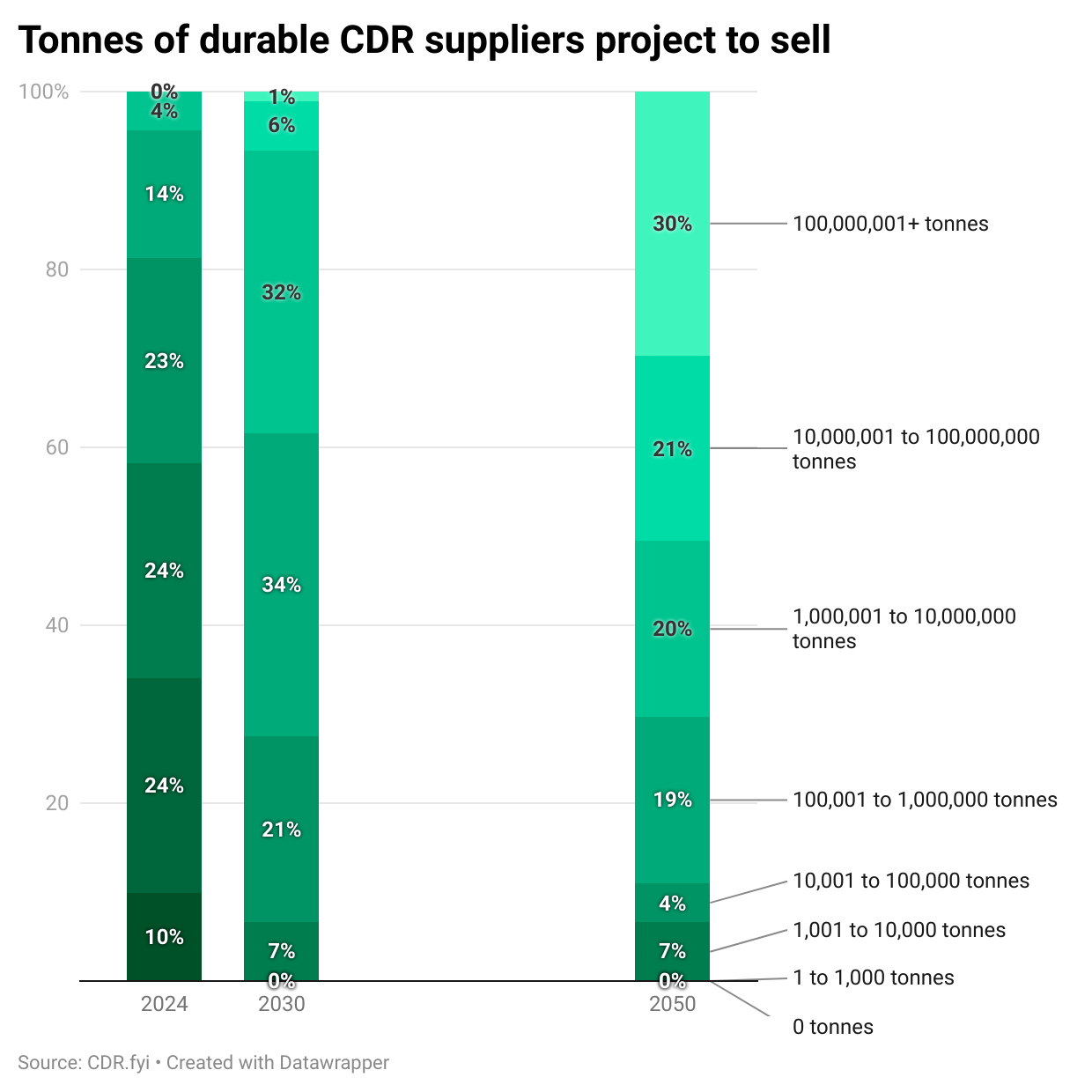

However, suppliers project rapid development in the coming years and leading to 2050. In 2024, 34% of suppliers project to sell 1,000 tonnes or fewer, a significant decrease from the 74% in that category for sales to date mentioned earlier. At these volumes and with the majority starting from a base of 0 tonnes, it is likely that many of these companies are in their early pilot phases. We also see 42% of suppliers stating they will sell over 10,000 tonnes in 2024, up markedly from the 14% who have done so thus far.

The growth-oriented outlook applies to future years as well. By 2030, 93% expect to exceed 10,000 tonnes, with almost 40% projecting more than 1M tonnes sold. By 2050, 70% project to sell more than 1M tonnes and 30% project to sell over 100M tonnes.

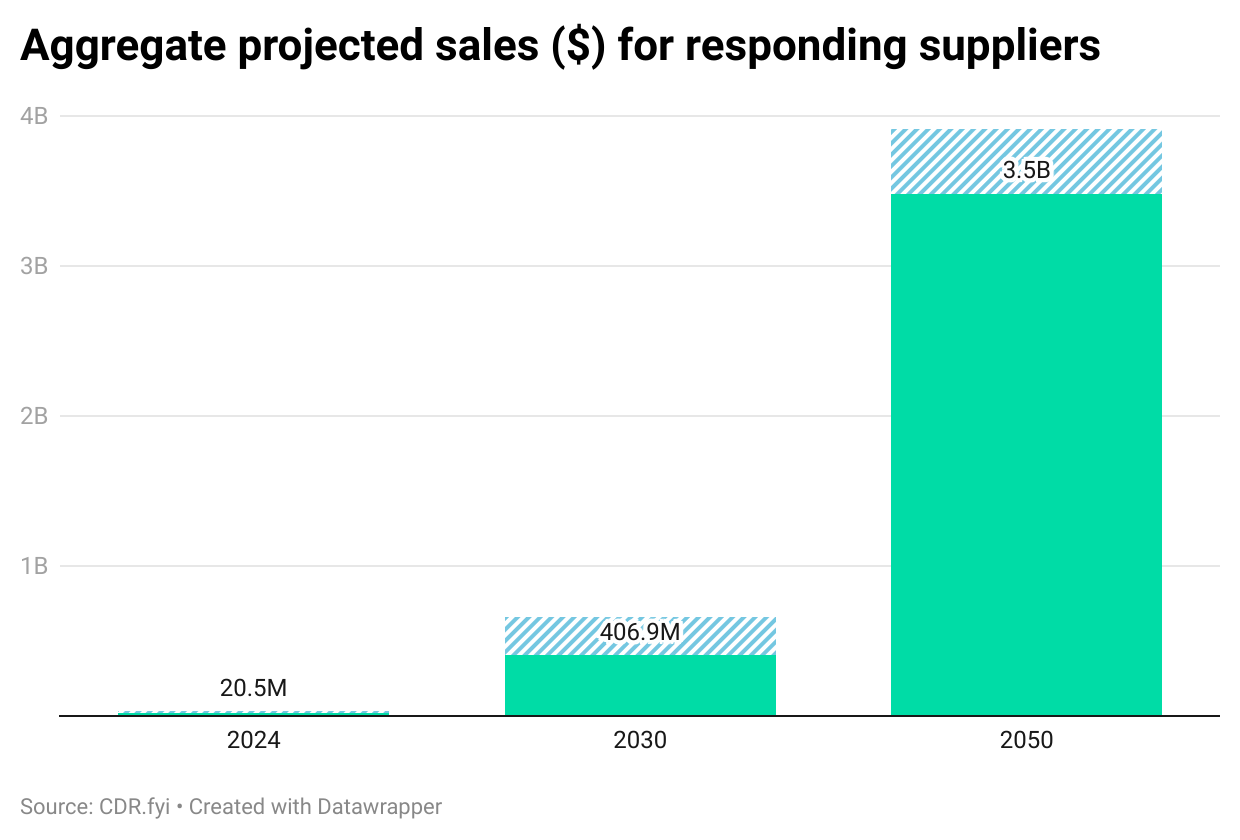

In aggregate, the 91 responding suppliers project sales between 9-31M tonnes in 2024, 253-660M tonnes in 2030, and over 3B tonnes in 2050.

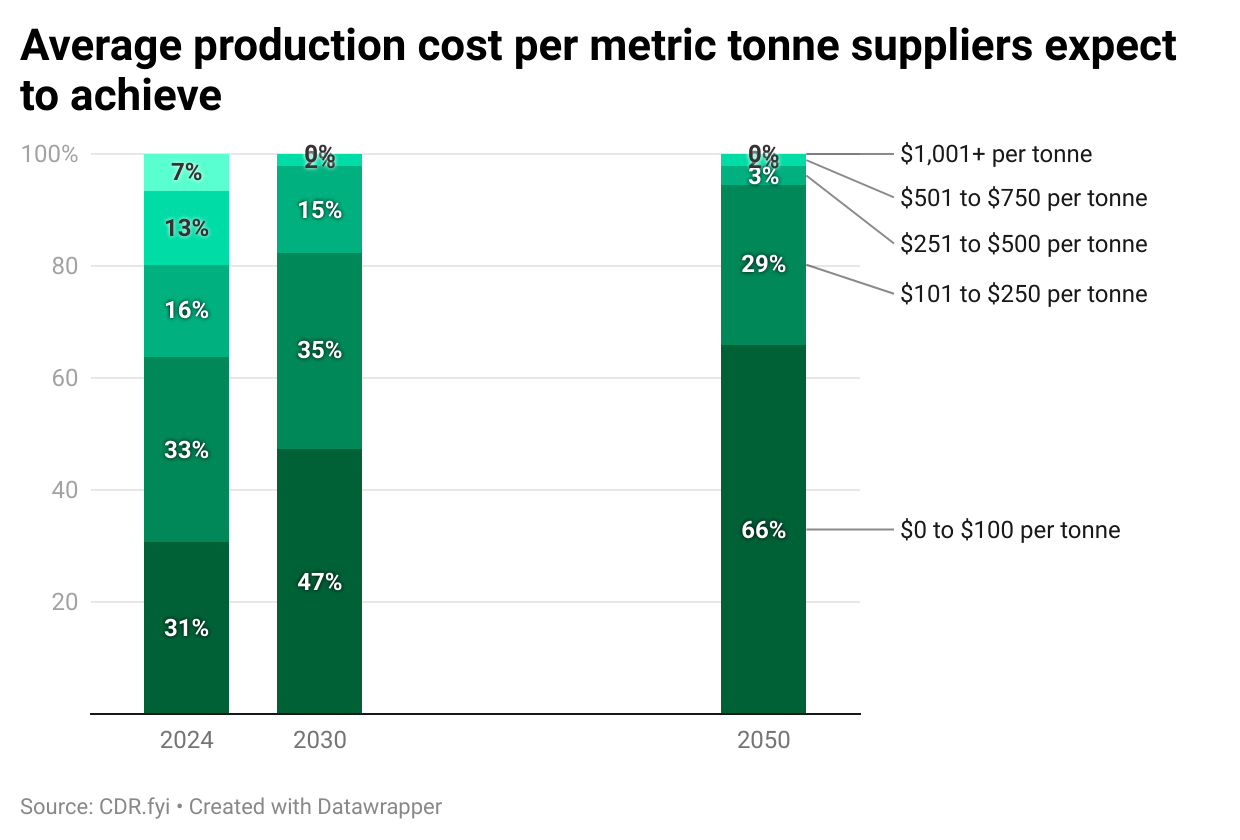

Cost Projections

As volumes rise, we expect to see costs come down. Nearly a third of suppliers see their cost per tonne under $100 in 2024, rising to two-thirds by 2050. At the higher end, 36% project costs over $250 per tonne in 2024, which eventually declines to 5% of respondents by 2050. Note that we asked about the cost of production, not the expected sales price.

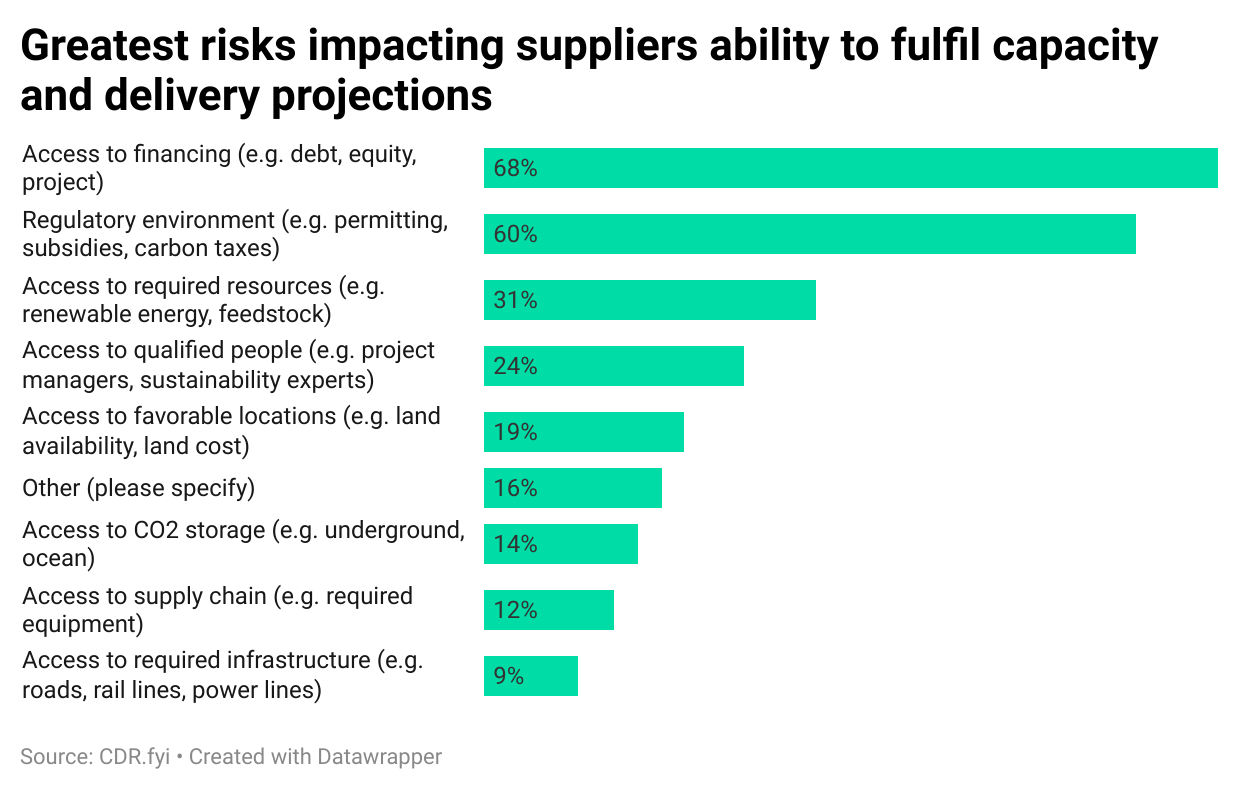

Risks

When asked what are the greatest risks to their projections, access to financing (chosen by 68% of respondents) and policy/regulatory challenges (60%) dominate the top risk factors. For example, one respondent mentioned “Political landscape / willingness to endorse and accelerate CDR” while another called out “Social licence to operate, favorable market forces and a supportive government that fosters innovation and climate action.”

Resource availability, hiring qualified staff, site selection, and infrastructure were also mentioned, but at a much lower level of concern.

While this question was intended to identify ancillary risks, the most common mention in the “Other” category (16%) was, not surprisingly, market demand. As one respondent said, “Someone to buy the CDRs is the number 1, 2,3,4 ... 1000 risk that we face.”

Channels

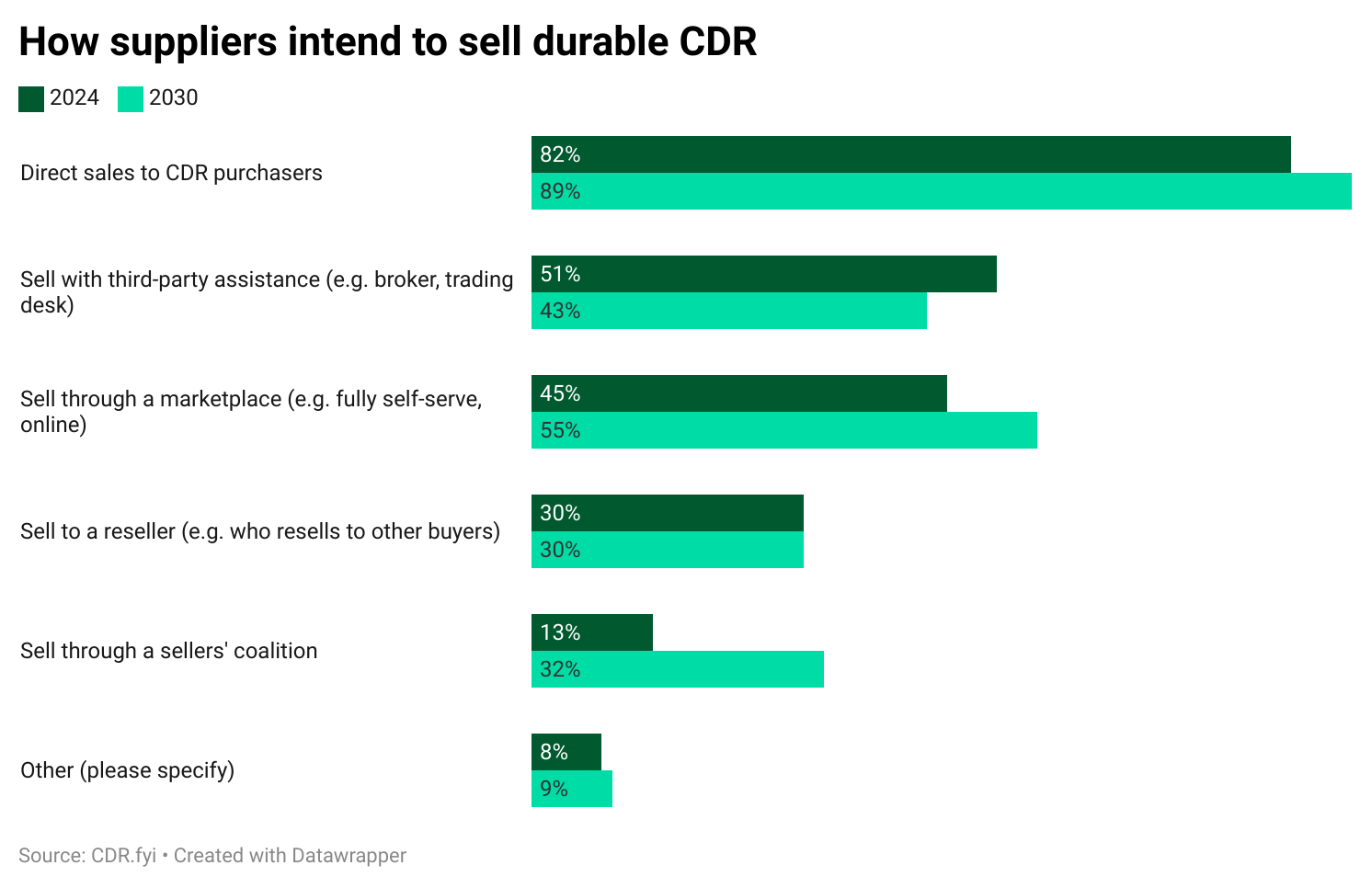

Interestingly, the channels that suppliers plan to use in 2024 and 2030 are very similar to those of purchasers. Direct sales stand out as the preferred channel: 82% in 2024 and 89% in 2030, compared to 63% in both years for purchasers. As with purchasers, marketplaces are the biggest upward movers from 2024 to 2030, rising from 45% to 55% for suppliers compared to 25% to 38% for purchasers.

One intriguing contrast between the purchase and supplier responses to this question is that suppliers selected approximately 50% more options than purchasers. Purchasers come across as more focused in their approach, while suppliers are likely anticipating trying a number of different channels to go to market and determining which ones work. Two comments from the “Other” selection underline this point: “We will sell to anyone that will buy them,” and “all the options will be experimented with.”

Profiles

Purchasers

The survey received responses from 27 organizations that purchased or planned to purchase durable carbon removal. Around half are based in the UK, US, or Canada, with another 30% from elsewhere in Europe. Most represent banking, IT, media, and related sectors.

The predominant purchaser profile comprises two segments: large companies with over $1 billion in revenue and early-stage startups. This likely reflects that organizations with higher profitability have a greater ability to pay for carbon removal, while startups are early movers in ESG initiatives.

Notably, 70% of respondents have already purchased some durable carbon removal, indicating that adoption is in the early but active stages.

Suppliers

Of the 91 supplier respondents, 66% of these companies were founded within the last three years, highlighting the rapid growth and burgeoning interest in the sector.

Geographically, the distribution of their headquarters mirrors what we observed in our 2023 Investment Landscape, with 22 companies based in the United States, 13 in Canada, and 9 in the United Kingdom.

Financially, most of these companies are in the early stages of revenue generation, with 71% reporting current revenues ranging from $0 to $1M and 91% having revenues under $10M.

Regarding workforce, 60% of these companies are in the 1 to 10-employee range, and 91% have fewer than 100 employees.

These profile responses paint the picture of a nascent industry primarily composed of small but rapidly evolving companies.

Methodology

This inaugural Market Outlook Survey comprised two separate questionnaires: one for purchasers and one for suppliers. The surveys were conducted in November and December of 2023.

The survey was about durable CDR specifically and those answering it were primarily durable CDR suppliers and purchasers that already bought or were interested in buying.

For clarity, we define “durable” as having a permanence of at least 100 years. Durable CDR covers methods such as biomass carbon removal and sequestration (BiCRS), biochar, bioenergy carbon capture and sequestration (BECCS), bio-oil sequestration, direct air capture (DAC), direct ocean removal, enhanced weathering, macroalgae, microalgae, macroalgae, and ocean alkalinity enhancement.

The results are directional and not a statistically significant reflection of the total group of suppliers and purchasers, especially not for the latter. For purchasers, the survey will reflect the views of current rather than future buyers since 99% of the purchasers who will eventually participate in this market have not yet done so.

Acknowledgements

For their tireless efforts in conducting the survey and analyzing the results to produce this Summary Report, we thank CDR.fyi team members Michael Guzzardi, Tank Chen, Quentin Servais-Laval, Kevin Niparko, Robert Höglund, and Alexander Rink.

For all of their guidance, input, and feedback on the 2024+ Market Outlook Survey, we give many thanks to: Eleonora Bacchi, Harris Cohn, Harry Connor, Sophie Dres, Vida Gabriel, Jason Grillo, Cimberley Groß, Mike Kelland, Claire Kiely, Joanna Klitzke, Annie Nichols, Markus Paff, Leo Park, Chris Podgorney, Axel Reinaud, Olivier Reinaud, Max Scholten, Mitchel Selby, Bjørnulf Tveit Benestad, and Antti Vihavainen. Special thanks to Peter Olivier, for having proposed to CDR.fyi the idea of a market outlook survey and its value to market participants.